Wellbeing One vs Wellbeing Two:

Comparison 2026

- By Willi Olsen

- Updated

The main difference is that Wellbeing One covers specialist consultations, diagnostic imaging, and tests only within six months after surgery, chemotherapy, or radiation, while Wellbeing Two provides the same cover without the six-month limit, offering greater flexibility and longer access to follow-up care.

Wellbeing One and Wellbeing Two are the two most popular health insurance plans offered by Southern Cross Health Insurance in New Zealand.

In contrast, Wellbeing Two provides the same benefits as Wellbeing One but removes the six-month time restriction, offering greater flexibility and extended coverage.

Wellbeing One vs Wellbeing Two

Southern Cross offers two health insurance plans: Wellbeing One and Wellbeing Two. Both cover surgical treatments and cancer care. Wellbeing Two provides broader benefits, including specialist consultations, diagnostic tests without time limits, and a $750 obstetrics allowance per claim year. Wellbeing One restricts these benefits to six months post-treatment and excludes obstetrics coverage.

What’s covered by Southern Cross’ Wellbeing One policy?

Southern Cross Wellbeing One is a comprehensive health insurance plan focused on surgical and healthcare needs. It reimburses 100% of eligible healthcare expenses up to the policy limit.

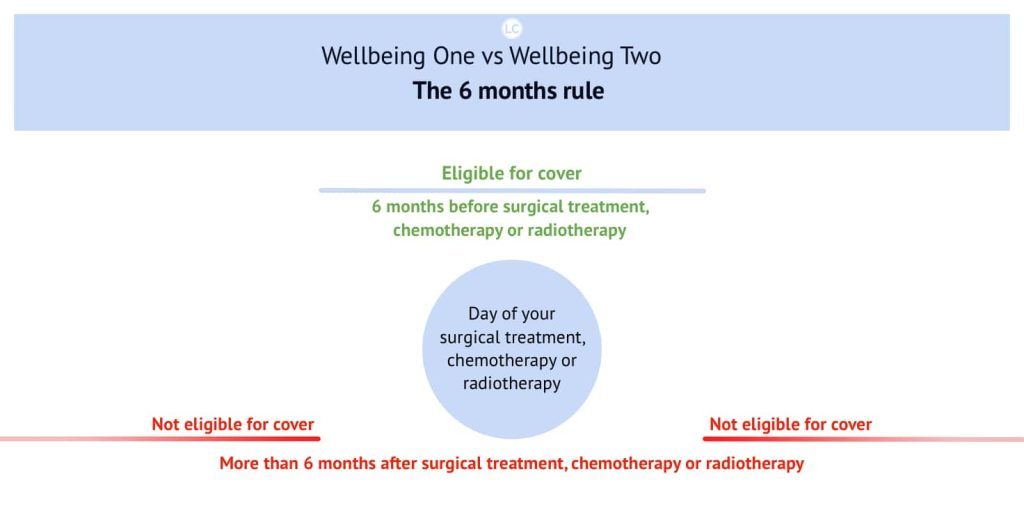

The plan includes a six-month rule. This means it covers diagnostic imaging and tests but only within six months of related eligible surgical treatment.

Key benefits of Wellbeing One include:

- Unlimited surgical treatment.

- Chemotherapy and unlimited radiotherapy.

- Specialist consultations.

- Diagnostic imaging and tests within six months of related eligible surgery.

This plan offers robust coverage, ensuring support for major health events.

What is the 6 months rule?

What’s covered by Southern Cross’ Wellbeing Two policy?

Southern Cross Wellbeing Two is a comprehensive health insurance plan that reimburses 100% of eligible healthcare expenses up to the policy limit. Unlike Wellbeing One, the six-month rule does not apply.

Key benefits include:

- Unlimited surgical treatment.

- Chemotherapy and unlimited radiotherapy.

- Specialist consultations.

- Diagnostic imaging and tests, regardless of surgery or treatment.

- Obstetrics allowance of $750 per claims year, available after one year of continuous cover.

What’s the difference?

Wellbeing Two offers the same core benefits as Wellbeing One. However, it also covers specialist consultations, diagnostic imaging, and tests without requiring surgery, chemotherapy, or radiotherapy. Additionally, it includes the obstetrics allowance, making it a more flexible and comprehensive option.

| Benefit | Wellbeing One | Wellbeing Two |

|---|---|---|

| Hospital & Surgical | ||

| Surgical treatment Private hospital, surgeon & anaesthetist fees | Unlimited Excess applies | Unlimited Excess applies |

| Chemotherapy for cancer Incl. $10,000 for non-Pharmac-funded drugs | $60,000 / year Excess applies | $60,000 / year Excess applies |

| Radiotherapy | Unlimited Excess applies | Unlimited Excess applies |

| Psychiatric hospitalisation | $3,500 / year | $3,500 / year |

| GP minor surgery e.g. ingrown toenails, steroid injections, abscess drainage | $1,000 / year | $1,000 / year |

| Skin lesion services Only $1,000 of this limit when performed by a GP | $5,000 / year | $5,000 / year |

| Overseas treatment allowance | $30,000 / year | $30,000 / year |

| Diagnostics & Follow-up — The Key Difference | ||

| Specialist consultations | $5,000 / year Within 6 months of related surgery only ² | $5,000 / year — no time limit |

| Diagnostic imaging MRI, CT scan, X-ray, ultrasound | $60,000 / year Within 6 months of related surgery only ² | $60,000 / year — no time limit |

| Diagnostic tests | $3,000 / year Within 6 months of related surgery only ² | $3,000 / year — no time limit |

| Cardiac tests | $5,000 / year Within 6 months of related surgery only ² | $5,000 / year — no time limit |

| Laboratory tests Non-government funded diagnostic tests | Not covered | $70 / year |

| Additional Benefits | ||

| Obstetrics allowance Available after 1 year of continuous cover | Not covered | $750 / year |

| Prophylactic treatment Available after 3 years of continuous cover | $40,000 lifetime | $40,000 lifetime |

¹ Excess applies to surgical treatment, chemotherapy, radiotherapy, recovery, psychiatric hospitalisation, and (Wellbeing Two only) obstetrics allowance. The excess is paid once per person, per claims year — regardless of how many claims are made. ² The 6-month rule: Under Wellbeing One, specialist consultations, diagnostic imaging, diagnostic tests, and cardiac tests are only covered when performed within six months of related eligible surgical treatment, chemotherapy, or radiotherapy. This restriction does not apply to Wellbeing Two. Important: This table is a general summary only. Terms, conditions, exclusions, and premium loadings apply. Please refer to the Southern Cross policy document for full details, or speak with a LifeCovered adviser for personalised guidance.

Regular Care Vs Wellbeing One and Two

The key difference between Regular Care and Wellbeing One lies in the excess structure and surgical benefits. Regular Care requires policyholders to pay 20% of the claim as an excess, whereas Wellbeing One sets a fixed excess amount, such as $500. Additionally, Regular Care caps the surgical benefit at $100,000 per operation, while Wellbeing One offers unlimited surgical coverage.

How does excess on Wellbeing One vs Wellbeing Two work?

Excess on Wellbeing One and Two is paid once every policy year, no matter how many times you claim. Therefore, the excess applies to each person on your policy once per claims year.

Which Wellbeing One and Two benefits does the excess apply to?

- Surgical treatment

- Surgical allowances

- Chemotherapy

- Radiotherapy

- Recovery

- Psychiatric hospitalisation

- Obstetrics allowance (Wellbeing Two only)

Your excess does not apply to any other benefits. Please see your policy document for full terms and conditions

Who is Southern Cross Health Insurance?

Southern Cross has been part of New Zealand’s healthcare story since 1961, when it introduced private health insurance to give Kiwis better access to medical treatment outside the public system. Set up as a not-for-profit, its goal has always been to make private healthcare more accessible and affordable for everyday New Zealanders.

Today, Southern Cross has grown into a group of health-focused businesses offering everything from health insurance and private hospitals to travel insurance, pet insurance, and life cover. It now supports the well-being of over one million Kiwis.

For employers, Southern Cross provides group health insurance designed to boost employee well-being and workplace benefits. These plans give staff faster access to private healthcare and help businesses improve retention and job satisfaction.

Two of the most popular plans are Wellbeing One and Wellbeing Two. Both include key benefits like cover for surgery, specialist consultations, and diagnostic tests. Wellbeing One offers essential cover, while Wellbeing Two steps it up with higher limits and broader coverage — a great choice for businesses wanting more complete protection for their teams.

FAQ's

What is excess?

An excess is an amount you will need to pay before SouthernCross will reimburse you or pay your health services provider for the eligible healthcare service you have received. You will pay the excess amount directly to your health services provider. The higher the excess amount, the lower your premiums will be.

Understanding excess options in Southern Cross wellbeing plans

The Wellbeing annual excess applies to both Wellbeing One and Wellbeing Two health plans from Southern Cross.

When setting up your policy, you can choose from five excess levels:

- Zero

- $500

- $1,000

- $2,000

- $4,000

These excess options give you flexibility – a higher excess typically lowers your premium, while a lower excess means paying more each month but less at claim time.

However, if you’re part of a workplace health insurance scheme, your employer may have set terms, and you might be unable to choose your excess level.

In other words, while Wellbeing plans offer personalisation through excess choice, your options may be restricted under group or employer-provided policies.

How does the excess apply?

The excess applies to each person on your policy once per claims year. So, if there are three members on your policy, all three will need to pay the excess each claims year before being reimbursed for any eligible healthcare services they receive. Once the full amount of each member’s excess has been applied, no excess will apply to any further claims by that member in that particular claims year.

What is a claims year?

Your claims year is the 12 months following your policy start date and every 12 months from your policy anniversary date. You can check this date in “My Southern Cross” and your Membership Certificate.

The claims year that applies to a particular claim is based on the date you received the healthcare service, not when you send Southern Cross your claim or when Southern Cross pay your health services provider.

At the beginning of each member’s new claims year, their excess will be reset to its original, full value.

Which Plan Is Right for You?

Both Wellbeing One and Wellbeing Two offer solid hospital and surgical cover, but the big difference comes down to how flexible they are when it comes to specialist consultations, diagnostic imaging, and follow-up tests.

- Wellbeing One keeps things simple and affordable — it’s ideal if you’re mainly after hospital cover and don’t expect much ongoing treatment after surgery or cancer care.

- Wellbeing Two gives you more breathing room. It covers specialists and follow-up testing without the six-month time limit, which is handy if you’re managing a chronic condition or want peace of mind long after your treatment ends.

If you’re healthy and just want the basics covered, Wellbeing One could be a good fit.

If you’d rather have more flexibility and fewer limits, Wellbeing Two might be worth the extra cost.

Not sure which plan suits you best?

Let’s have a quick yarn about what’s right for your needs – I’ll compare the best health plans from Southern Cross, Partners Life, nib and more – so you can feel confident you’re sorted.

Looking for health insurance?

Need help finding the right cover?

Call 0800 259 925 or book a time we’re here to make insurance simple and stress-free.

Disclaimer: The information in this article is for general guidance only and does not replace personalised financial advice. While every effort has been made to ensure the content is accurate and relevant, insurance policies, healthcare benefits, provider offerings (including nib, Partners Life, and others), and regulatory settings may change over time. This article may not reflect your circumstances or the latest industry updates. We recommend you speak with a qualified and licensed financial adviser for advice tailored to your situation. LifeCovered is here to help – our advisers are fully licensed and experienced in providing personalised insurance and financial guidance.

How much does our advice cost?

LifeCovered does not charge any fees for our service.

We provide unbiased advice by looking at all your insurance options across different providers – and our service is completely free. We’re paid through commissions by the insurance companies, who share a portion of their margin with us as your financial adviser. You’ll pay exactly the same premium whether you use our expert advice or go directly to the insurer. That means you get professional, impartial guidance to help you make informed decisions at no extra cost.