You can lock in fixed premiums, that don’t increase with age for 30 or 40 years.

Premiums that don’t increase with age is unknown to most New Zealanders.

There’s a couple of reasons for that.

First, most frontline workers at the main banks wouldn’t know anything about them, nor do many of the banks have any of these options available.

Second, they are not as profitable for the banks and insurers.

Advisers and retailers are rarely rewarded the same for providing these fixed premiums to clients.

In general, someone with a fixed premium cover will keep their insurance in place for a much longer time, than someone with a ‘stepped’ – ‘increasing’ premium cover, because the fixed one, is so much more affordable.

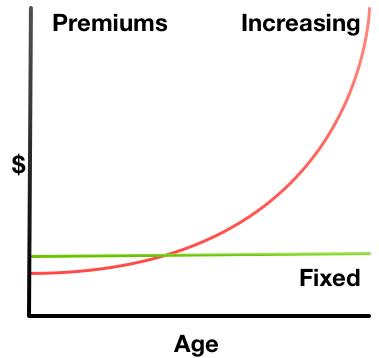

See the graph showing the difference.

Level rates will normally save you tens of thousands over the lifetime of the policy.

Furthermore, you will know what the cover will cost you over the long term.